Let’s dig into the relative performance of DexCom (NASDAQ:DXCM) and its peers as we unravel the now-completed Q4 patient monitoring earnings season.

Patient monitoring companies within the healthcare equipment industry offer devices and technologies that track chronic conditions and support real-time health management, such as continuous glucose monitors (CGMs) and sleep apnea machines. These businesses benefit from recurring revenue from consumables and software subscriptions tied to device sales (razor, razor blade model). The rising prevalence of chronic diseases like diabetes and respiratory disorders due to an aging population as well as growing adoption of digitization are good for the industry. However, these companies face challenges from high R&D costs and reliance on regulatory approvals. Looking ahead, the sector is positioned for growth due to tailwinds like the rising burden of chronic diseases from an aging population, the shift toward value-based care, and increased adoption of digital health solutions. Innovations in AI and machine learning are expected to enhance device accuracy and functionality, improving patient outcomes and driving demand. However, there are headwinds such as pricing pressures as healthcare costs are a key focus, especially in the US. An evolving regulatory landscape and competition from more tech-forward new entrants could present additional challenges.

The 4 patient monitoring stocks we track reported a strong Q4. As a group, revenues beat analysts’ consensus estimates by 1.9% while next quarter’s revenue guidance was 1.9% below.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 14.9% since the latest earnings results.

Founded in 1999 and receiving its first FDA approval in 2006, DexCom (NASDAQ:DXCM) develops and sells continuous glucose monitoring systems that allow people with diabetes to track their blood sugar levels without repeated finger pricks.

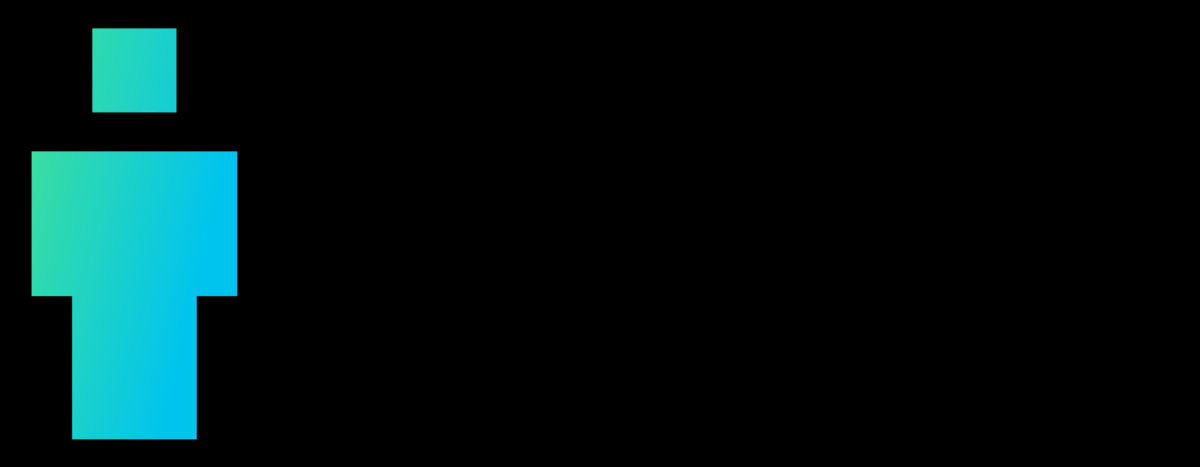

DexCom reported revenues of $1.26 billion, up 13.1% year on year. This print exceeded analysts’ expectations by 0.8%. Despite the top-line beat, it was still a mixed quarter for the company with a beat of analysts’ EPS estimates but full-year revenue guidance meeting analysts’ expectations.

DexCom Total Revenue

DexCom delivered the weakest performance against analyst estimates and weakest full-year guidance update of the whole group. The stock is down 1.5% since reporting and currently trades at $64.12.

Pioneering the shift from bulky, short-term heart monitors to sleek, wire-free patches, iRhythm Technologies (NASDAQ:IRTC) provides wearable cardiac monitoring devices and AI-powered analysis services that help physicians detect and diagnose heart rhythm disorders.

iRhythm reported revenues of $208.9 million, up 27.1% year on year, outperforming analysts’ expectations by 3.4%. The business had a very strong quarter with a beat of analysts’ EPS and revenue estimates.

iRhythm Total Revenue

iRhythm scored the biggest analyst estimates beat and highest full-year guidance raise among its peers. Although it had a fine quarter compared its peers, the market seems unhappy with the results as the stock is down 27.4% since reporting. It currently trades at $115.27.

Founded in 1989 to address the then-underdiagnosed condition of sleep apnea, ResMed (NYSE:RMD) develops cloud-connected medical devices and software solutions that treat sleep apnea, COPD, and other respiratory disorders for home and clinical use.

ResMed reported revenues of $1.42 billion, up 11% year on year, exceeding analysts’ expectations by 1.6%. It may have had the worst quarter among its peers, but its results were still good as it also locked in a decent beat of analysts’ revenue estimates and a beat of analysts’ EPS estimates.

ResMed delivered the slowest revenue growth in the group. As expected, the stock is down 10.9% since the results and currently trades at $229.51.

Revolutionizing diabetes care with its tubeless “Pod” technology, Insulet (NASDAQ:PODD) develops and manufactures innovative insulin delivery systems for people with diabetes, primarily through its Omnipod product line.

Insulet reported revenues of $783.8 million, up 31.2% year on year. This result surpassed analysts’ expectations by 2%. It was a strong quarter as it also logged a solid beat of analysts’ revenue estimates and a beat of analysts’ EPS estimates.

Insulet achieved the fastest revenue growth among its peers. The stock is down 19.9% since reporting and currently trades at $197.31.

Late in 2025 into early 2026, there was hand wringing around artificial intelligence. For software companies, the fear was that AI would erode pricing power and compress margins as new tools made it easier to replicate what once required expensive enterprise platforms. Crypto investors had their own version of the same anxiety: if AI agents could trade, allocate capital, and manage wallets autonomously, what exactly was the long-term value of today’s crypto infrastructure?

These concerns triggered a noticeable rotation away from these sectors and into safer havens. But markets rarely dwell on one narrative for long. Spring 2026 came, and the focus shifted abruptly from technological disruption to geopolitical risk. The US’ conflict with Iran became the dominant driver of market psychology, and when geopolitics takes center stage, the script changes quickly. Investors stop debating growth rates and start worrying about oil supply, inflation, and global stability.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Quality Compounder Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.